By Misyrlena Egkolfopoulou

Crypto had already been seeping into every corner of culture and conversation. Then came Russia’s invasion of Ukraine, and crypto went to war, too.

The sector’s involvement in the war has showcased the development and maturity of digital assets while reviving — without resolving — the debate about their role in the global financial system. As Russia invaded Ukraine, the world participated real-time in the financing of a standing army with cryptocurrency donations that funded military supplies for Ukraine. Digital currencies lived up to their reputation for easily moving money across international borders but simultaneously set off a debate about whether they can be used to evade sanctions.

Meanwhile, crypto exchanges were thrust into the spotlight as the industry grappled with decisions on whether the restrictions imposed by Western nations applied to them and how to monitor transactions of certain customers. And as markets felt the pressure of worldwide uncertainty over the war, cryptocurrencies emerged — at least initially — as safe havens, highlighting their potential power to minimize the importance of the dollar-run world.

“This moment has really emphasized the best parts of crypto but also reinforced some of the areas that still need work,” said Stephanie Hurder, partner and founding economist and Prysm Group, an economic advisory focused on blockchain and distributed ledger projects. “There’s promise in the transfer of value but a lot of the issues that we know exist are really still there.”

Since the invasion began, two financial systems have been playing out in tandem: the traditional and the digital. The former rendered Russia a financial pariah by subjecting it to harsh sanctions that cut it off from the global financial system. U.S. President Joe Biden’s administration banned individuals and companies from doing business with the central bank of Russia and excluded major Russian banks from the SWIFT financial messaging service in coordination with European allies.

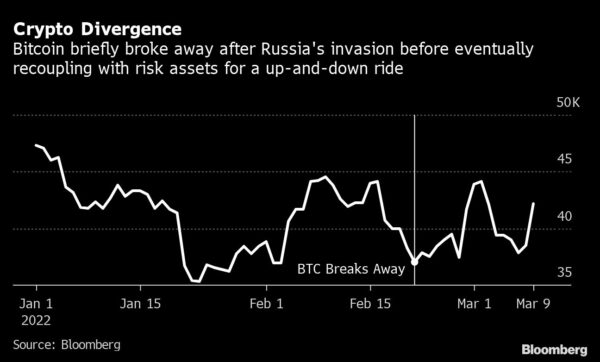

In crypto markets, Bitcoin surged as much as 20% at the start of last week, topping $45,000 for a moment even as risk assets slumped on speculation that sanctions and a collapsing ruble would drive Russians into cryptocurrencies. Although Bitcoin later gave up almost all of those gains, the coin’s divergent path from speculative securities, while brief, renewed the debate about its role in the global financial system. Its return to earth shows the debate is far from settled.

“The conflict is bringing a tremendous amount of attention on the cryptocurrency industry, full stop,” said Alex Zerden, an Adjunct Senior Fellow at the Center for a New American Security. “A lot of people want to see what is going on to perpetuate their narrative or their views with respect to crypto. It’s reinforcing narratives, it’s not converting narratives right now.”

Bitcoin was born in the wake of the global financial crisis as an alternative currency outside the traditional monetary system. Since that time, it has been promoted as a means of exchange, an inflation hedge and a store of value that is detached from governmental control. As soon as sanctions were imposed, trading volumes in Bitcoin using the ruble surged to the highest level since May, while those based in Ukraine’s hryvnia climbed to a level not seen since October, according to crypto data firm Kaiko. To be sure, the volumes were still relatively small.

“If you’re in Russia or Ukraine right now, I don’t think Bitcoin’s volatility is actually going to be that much of a concern to you relative to your political and economic volatility,” said Matthew Pines, a fellow at the Bitcoin Policy Institute. “It’ll help folks protect their wealth from the collapsing ruble, put it in a form that’s hard for the Russian government to seize and even maybe help them get it out of the country in the first place.”

Cryptocurrency has been used as a peer-to-peer payment to support activists in a number of countries, because of the ease of the open source wallets that can be downloaded directly to people’s phones. Once set up, a wallet address can receive funds in the form of crypto from anyone in the world, including family members and relatives. But the conversion to fiat currencies can impose a practical layer of friction for people in a conflict zone, who will need to have internet access to ensure their smartphones are properly set up.

“If you want to use it to go buy some lunch and that merchant doesn’t accept Bitcoin then you have to convert it into local currency,” Pines said. “It does depend on where you are and it depends on exactly how stable the jurisdiction is.”

The brief rally also led to speculation around whether cryptocurrencies might be used to skirt the sanctions the U.S. and its NATO allies put on Russia. Even politicians voiced that concern, with Massachusetts Senator Elizabeth Warren saying crypto is “a shadow world” that Russians and other countries can use to help “sanction-proof” themselves. FTX CEO Sam Bankman-Fried and Brett Harrison, president of the exchange’s American arm, pushed back on the idea.

Exchanges like FTX and other crypto firms were also thrust into the spotlight, trying to figure out how to deal with western sanctions against Russia after its invasion of Ukraine. Crypto exchanges based in jurisdictions beyond the scope of sanctions and others that don’t require customer identification were left wondering how to impose curbs for their customers. What’s more, some firms aren’t entirely sure how to even comply with the restrictions, given the blurry regulatory framework that oftentimes applies to cryptocurrencies.

“A lot of the potential limitations of crypto or benefits of it is going to hinge on how exchanges decide to regulate and impose sanctions,” said Prysm’s Hurder.

Clarity in regulations may help define digital assets’ role — and it’s coming, though not imminently. On Wednesday, Biden signed an executive order calling for a government-wide approach to crypto oversight, with agencies working together. But it also mandated a series of studies on the sector that may take up to a year. Globally, regulation remains patchy.

Crypto has perhaps been most conspicuous since the invasion as a vehicle for fundraising, and in that role it has been quite successful. With a QR code or a string of characters, digital currencies have become the vehicle of choice for many and a low-friction way for individuals and groups who wanted to raise money. So far, the Ukrainian government has raised more than $60 million, through more than 118,000 donations, according to Elliptic, a blockchain analytics firm.

The Ukrainian government’s organized outreach not only raised money, but rallied people all over the world to buy in to their war efforts and encourage other people to engage with crowds on social media. As with everything in crypto, though, there are two sides to the story.

“For the first time in history, a country’s military budget now depends on the quality of the memes that this country can produce,” said Dror Poleg, founder of Hype Free Crypto, a crypto online education platform. “But the mechanism itself is terrifying because tomorrow who knows what people on Twitter are going to get excited about or want to finance.”

The future of money may be in flux, but the debate over crypto remains wide open.

More stories like this are available on bloomberg.com.